How Interest Works in Bank Accounts: A Simple Beginner Guide

How Does Interest Work in Bank Accounts

When I first viewed my bank statement and saw a modest additional amount charged as “interest,” I didn’t notice it. It wasn’t much, and I wasn’t sure where it came from. At the time, I believed that interest was primarily important for individuals with significant funds. Years later, when I began to pay more attention to my finances, I understood that knowing how interest works in bank accounts is about awareness and habit, not the amount.

This guide discusses interest in simple terms, without technical jargon.

What Is Interest on a Bank Account?

Interest is the amount of money a bank pays you for keeping your money with them.

In simpler terms:

• Deposit money at a bank.

• The bank utilizes the funds for lending.

• The bank provides interest in return.

Understanding how interest works in bank accounts explains why banks reward saves.

Why do banks pay interest?

Banks do not hold your money idle.

They:

- Lend money to others.

- Invest funds safely.

- Maximize profit from interest differential.

A tiny portion of the earnings is distributed to you as interest.

Bank Accounts that Earn Interest

Not all bank accounts generate interest in the same manner.

Accounts that often yield interest include:

• Savings accounts.

• Fixed deposits.

• Recurring deposits.

Savings accounts are the most regularly utilized.

How is interest calculated in bank accounts?

Interest calculation may appear difficult, but the concept is straightforward.

Banks compute interest using:

• Account balance.

• Interest rates

• Time period.

Despite the fact that interest is credited monthly or quarterly, most savings accounts calculate the amount daily.

The Daily Balance Method Explained Simply

Daily balance means:

• The bank checks your balance daily.

• Interest is computed on the daily amount.

• Final interest is added occasionally.

This strategy favors steady balances over random deposits.

What Does Interest Rate Really Mean?

The interest rate is the proportion of your balance paid in interest each year.

For example:

• 3% interest is ₹3 every ₹100 in one year.

Rates vary between institutions and might alter over time.

My Personal Lesson On Interest

For years, I withdrew funds as soon as they were credited. My equilibrium was rarely solid. One month, I decided to leave a portion undisturbed. When interest was credited the next time, it seemed modest but significant. That modest benefit taught me to be patient. I recognized that interest rewarded consistency over hurry.

That’s when the notion of how interest works in bank accounts became a reality.

A Simple Example of Interest in Savings Account

Let us take a basic example.

If you save ₹50,000 in a savings account at 3% interest:

• Annual interest: ₹1,500 (about).

• Monthly impact is little.

• Prioritize long-term habits.

The sum may not appear big, but it fosters discipline.

Compound Interest vs Simple Interest

Interest can work in two ways.

Simple Interest

Calculated only on the original amount.

Compound Interest

Calculated on original amount plus previously earned interest.

Savings accounts benefit slightly from compounding over time.

Why Interest in Savings Accounts Feels Low

Many people feel savings interest is too low.

Reasons include:

- High liquidity (easy access)

- Low risk

- Short-term use

Savings accounts focus on safety, not high returns.

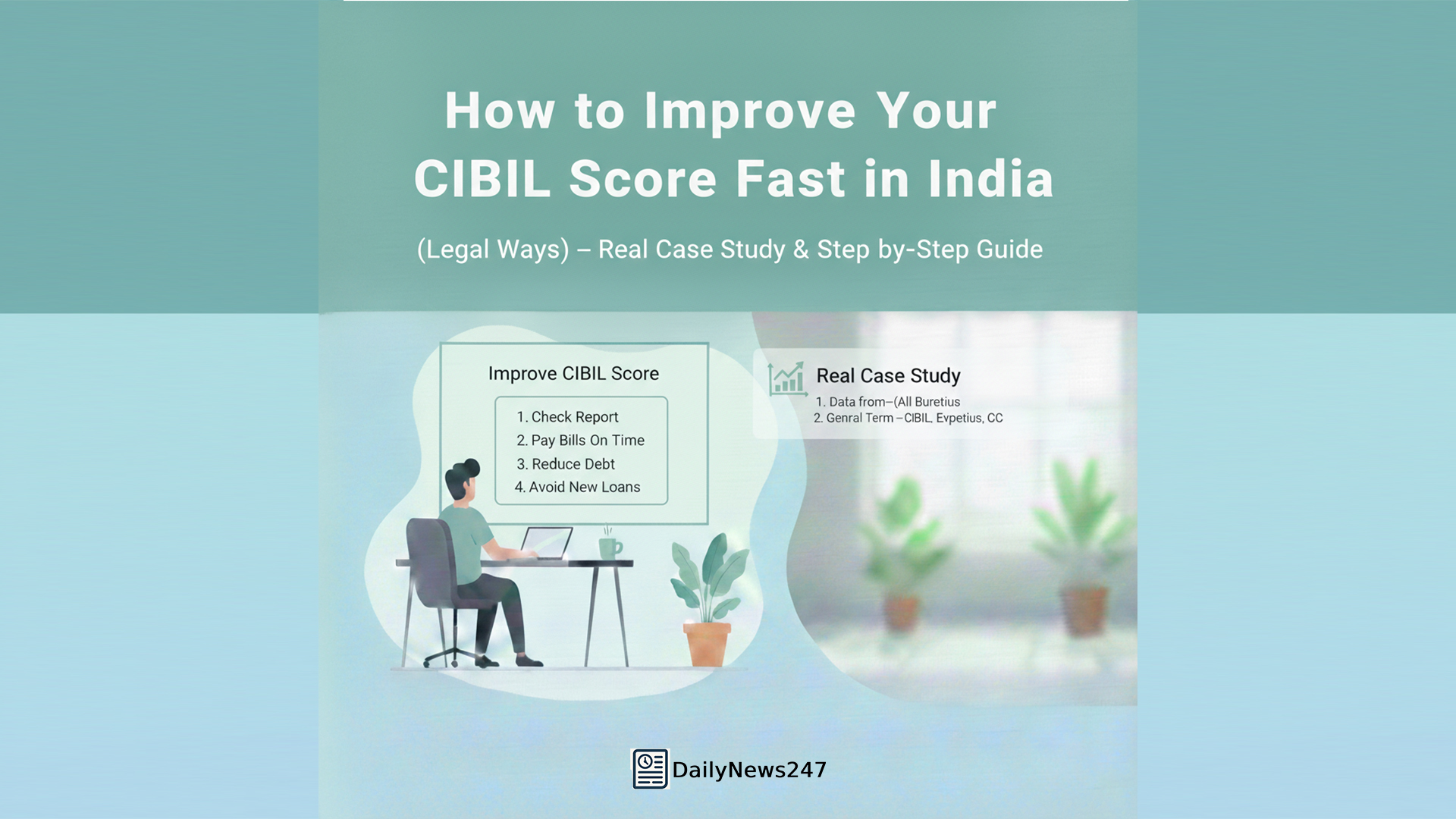

How to Earn More Interest From Bank Accounts

You may boost interest effect by:

• Maintaining a higher balance.

• Choosing favorable interest rates.

• Preventing frequent withdrawals.

Small modifications offer long-term results.

Common Myths about Bank Interest

Many individuals misinterpret the concept of interest.

Common Myths:

• Only wealthy individuals prioritize their interests.

• Small balances earn nothing.

• Interest is not worth tracking.

These ideas undermine sound savings habits.

Tax on Interest Earned

Interest earned may be taxed, depending on the regulations.

Important Points:

• Interest is classified as income.

• Tax regulations differ based on account type and amount.

Understanding this helps to avoid surprises later.

Savings Accounts versus Fixed Deposit Interest

Savings Account:

• Lower interest.

• Easy access.

Fixed Deposit:

• Higher interest.

• Locked for a while.

Each has a distinct purpose.

Why Understanding Interest is Important for Beginners.

When novices learn how interest works in bank accounts, they:

• Develop saving habits.

• Improve banking choices.

• Appreciate consistency.

Knowledge enables control.

How Interest Impacts Financial Planning

Interest has a subtle but significant impact in:

• Emergency funding.

• Short-term savings.

•Ignoring financial stability might result in missed opportunities.

FAQs – Bank Account Interest

- How often is interest credited in savings accounts?

Usually monthly or quarterly, depending on the bank.

- Does withdrawing money reduce interest?

Yes, lower balances reduce interest earnings.

- Is interest guaranteed in savings accounts?

Interest rates may change, but savings accounts are considered low risk.

Share this content:

Post Comment